Blog

05 15, 2026

{{ content.title }}

{{ content.description }}

On April 28, 2026, the Midcontinent Independent System Operator (MISO) released the results of their Planning Resource Auction (PRA) for the 2026/2027 planning year. The outcome is in stark contrast to the 2025/2026 results, where pricing soared 10x and summer pricing soared 22x due to supply concerns caused by power plant suspensions/retirements, reduced accreditation of resources, growing demand, and the implementation of a new demand curve model. This time around, available capacity is outpacing demand. As a result, pricing in MISO’s capacity market plunged.

In this blog, we break down the key drivers behind the auction results. We also explore how exclusive utility relationships across MISO are helping deliver demand response pricing stability while positioning participants for long-term success in the market.

The basics of the PRA

Before we dive into the results, it’s important to level set and understand that MISO’s PRA differs from capacity auctions in other regions. For example, PJM’s capacity auction, the Base Residual Auction, is responsible for securing most of the region’s capacity needs and is held by PJM well in advance, with Incremental Auctions following the main auction to tie up any loose ends.

The PRA, on the other hand, occurs right before the start of the planning year, June 1, because its purpose is to ensure there are no last-minute capacity shortfalls. MISO is comprised largely of vertically integrated, regulated utilities – known as Load Serving Entities (LSEs) – and most of them self-supply their own capacity or secure it in advance of the PRA. Those that have capacity shortfalls leverage the PRA to fill any gaps.

The results of the 2026/2027 PRA

The 2026/2027 PRA is the second year that MISO has used a sloped demand curve in the auction, rather than the vertical demand curve they used before 2025/2026. The sloped demand curve delivers a pricing structure that accurately reflects the reliability value of capacity above and below resource adequacy targets, directly tying capacity prices to reliability value. It also helps improve price signals, stabilize prices, and avoid the extreme volatility historically seen in a vertical demand curve.

MISO cleared sufficient resources in this auction to meet reliability requirements, and price signals continue to vary dramatically across seasons, just as they did in the previous auction.

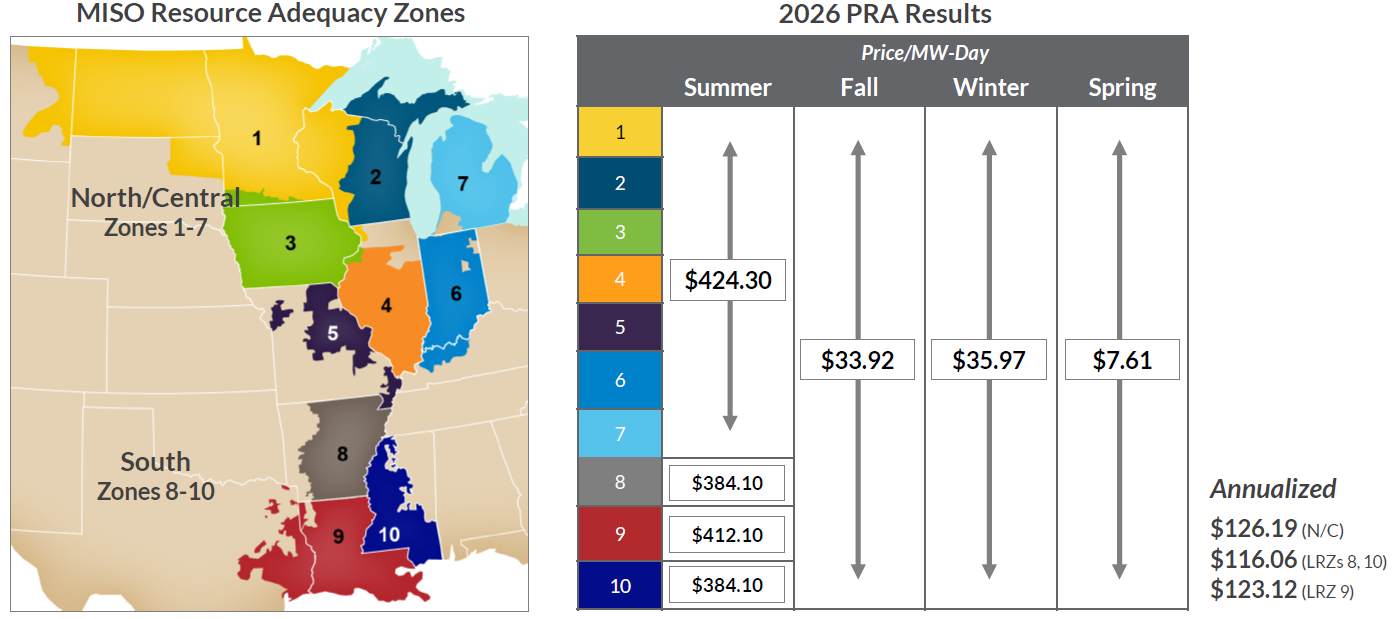

MISO PRA 2026/2027 seasonal clearing prices by zone

Source: MISO Planning Resource Auction Results for Planning Year 2026/27

However, these prices are much lower than the 2025/2026 auction prices. Let’s compare:

Season | 2026/2027 | Compared to 2025/2026 |

Summer (June, July, August) | Zones 1-7: $424.30/MW-day | A decrease from $666.50/MW-day across all zones |

Fall (September, October, November) | All zones: $33.92/MW-day | A decrease from $91.60/MW-day in zones 1-7 and $74.09/MW-day in zones 8-10 |

Winter (December, January, February) | All zones: $35.97/MW-day | A slight increase from $33.20/MW-day across all zones |

Spring (March, April, May) | All zones: $7.61/MW-day | A decrease from $69.88/MW-day across all zones |

Annualized averages see pricing drop by nearly half across every zone:

Zone | 2026/2027 | Compared to 2025/2026 |

Zones 1-7 | $126.19/MW-day | A decrease from $217/MW-day |

Zone 8 | $116.06/MW-day | A decrease from $212/MW-day |

Zone 9 | $123.12/MW-day | A decrease from $212/MW-day |

Zone 10 | $116.06/MW-day | A decrease from $212/MW-day |

Why did prices decrease?

Leading up to the PRA, MISO expressed concerns about resource adequacy. After all, MISO is one of the regions experiencing unprecedented load growth, driven primarily by new “large, concentrated loads” from data centers, AI, and manufacturing, as expressed in their latest long-term forecast on April 13, 2026. In this report, MISO estimates that peak load across the region will grow from 121 GW in 2025 to 163 GW by 2035 – an increase of 35%. They expect 8 GW to 14 GW of data centers to come online in 2026 and 2027 alone, and this growth will be a key indicator of how quickly data center-driven demand can materialize.

Given these forecasts, there was every reason to expect that the outcome of the 2026/2027 PRA would tell a similar story to 2025/2026 – high demand forecasts, tight reserve margins, and generation assets retiring, all resulting in high pricing. However, two unexpected occurrences happened as the auction drew closer:

- In late February and early March, new solar capacity came online and was available to be offered into the auction.

- Generation assets set to be decommissioned pre-auction were delayed.

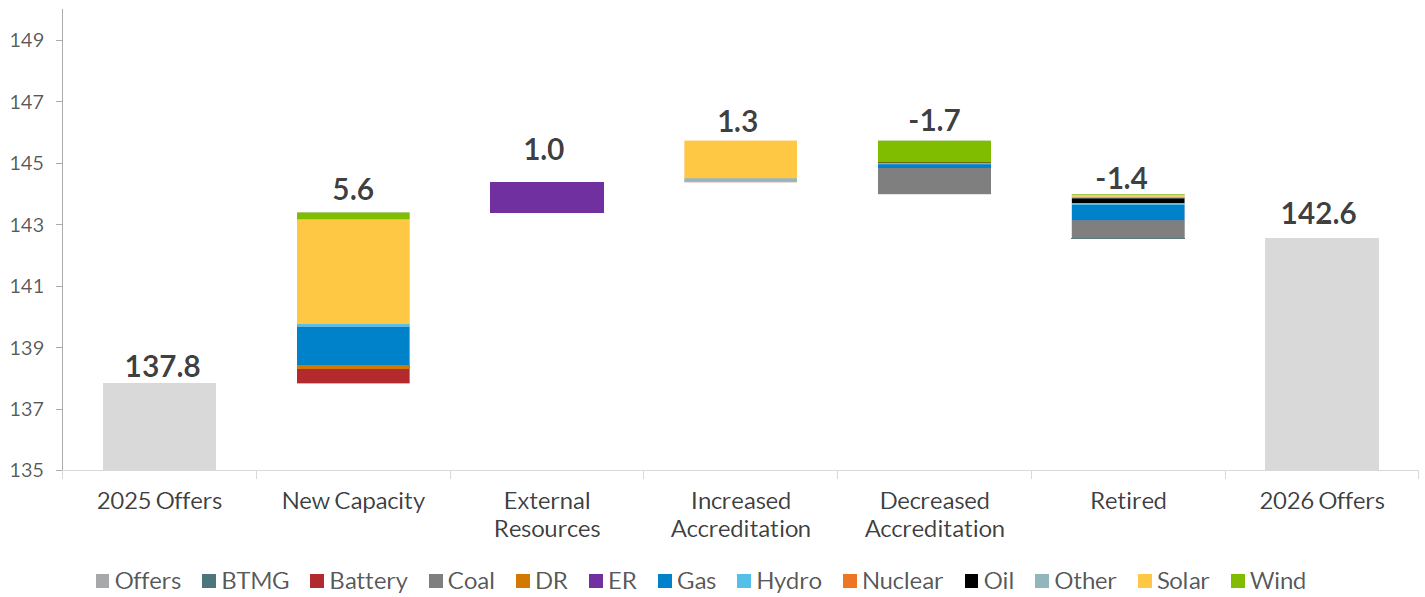

As a result, new capacity additions in this auction – mostly from the new solar assets mentioned above – outpaced decreases in accreditation and retirements, as shown in the diagram below. Capacity offered for the summer increased by about 4%, jumping from 137.8 MW in 2025 to 142.6 GW in 2026.

Capacity offered summer 2026 versus summer 2025 (GW)

Source: MISO Planning Resource Auction Results for Planning Year 2026/27

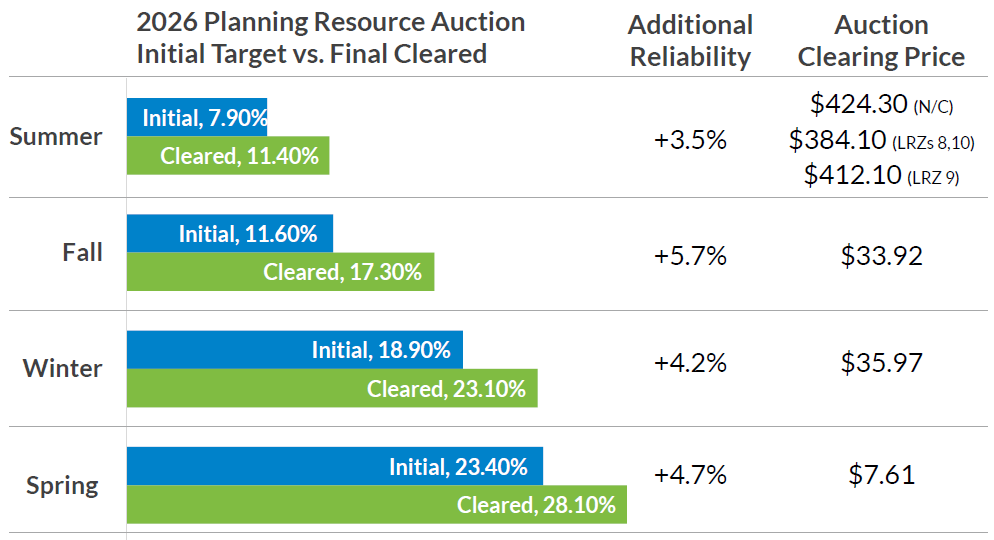

All four seasons cleared well above their reserve margin targets – that extra cushion beyond what’s needed to meet forecasted demand, so that MISO can handle unexpected demand spikes or generation outages.

That said, summer pricing reflects the highest reliability risk, since supply during this season remains tight. As a result, most of the value in the auction is concentrated in the summer season, mainly across zones 1-7.

Source: MISO Planning Resource Auction Results for Planning Year 2026/27

What do these results mean for the demand response market in MISO?

First things first, as mentioned at the start of this blog, most Load Serving Entities (LSEs) in MISO are self-supplying and securing their own capacity before the PRA, so they are unaffected by these lower prices. According to MISO’s auction results, about 92% of these entities secured their capacity outside of the auction, leaving just 8% affected by the auction pricing.

Second, while MISO secured sufficient capacity to meet their reserve margin requirements, they remain concerned about load growth. They mentioned in their auction results that “New generation capacity is coming online, but faster resource additions are still needed to support large-load growth and ensure resource adequacy.” Flexible capacity that can dynamically control the demand side of the energy equation remains essential to maintaining grid reliability, with demand response programs playing a critical role in delivering that flexibility.

As a result, utilities in MISO are finding avenues outside the PRA to meet load growth expectations, taking matters into their own hands to support the energy transition and ensure grid reliability by offering their own demand response programs to their customers. These utilities are proactively securing and reserving blocks of capacity for their customers – and offering more competitive, reliable, and stable demand response pricing in contrast to PRA price volatility. They then establish a bilateral relationship with a preferred demand response provider to help their customers enroll and participate in the program.

With the lower PRA pricing set to take effect June 1, 2026, businesses in MISO can be well served by working with a demand response provider that can grant them access to these competitive, exclusive programs. Enel North America offers exclusive, bilateral utility programs with Ameren Illinois, Ameren Missouri, CenterPoint Energy in Indiana, and Entergy Louisiana – and we are actively pursuing more programs that provide predictable, competitive prices for businesses looking to participate in the market.

These utilities selected Enel North America to serve their programs due to our demonstrated expertise in delivering value to our customers. Demand response should be predictable, rewarding, and low-hassle. Backed by more than 20 years of experience and a global track record as the largest demand response provider, we help businesses in MISO and across North America:

- Identify and capture demand response opportunities

- Maximize demand response revenue with full transparency

- Navigate market complexity with expert guidance

- Avoid demand response penalties through proven performance

Enel’s customer-first approach, advanced technology, and unmatched expertise make us the trusted partner for businesses ready to lead in a smarter energy future. Contact us today to get a conversation started with our team.